A borrower uploads documents at 9:12 PM. A pay stub, bank statement, tax return, and ID. By 9:13 PM, one lender has acknowledged receipt and started processing. By the next morning, the borrower has a conditional approval.

Another lender doesn’t even open the file until 10:30 AM the next day.

Same borrower. Same documents. Two very different outcomes. In most cases, that borrower doesn’t wait. They go with the first lender.

This is where slow document processing starts to hurt real business metrics:

- Lower pull-through rates because borrowers drop off mid-process

- Slower portfolio growth despite strong lead volume

- Higher cost per funded loan due to wasted acquisition effort

- Longer time-to-decision, reducing competitiveness

Manual document review is not just a cost center. It is a conversion problem. AI-powered document processing changes this dynamic by reducing decision time from days to hours. Intelligent document processing for loans, combined with AI agents, eliminates wait times in the system. Not entirely, but enough to matter.

Enterprises implementing automation in lending have reported 200% to 300% return on investment within the first year, while document processing time has decreased by nearly 60% to 70% as manual data entry is reduced.

This blog is for fintech founders, SME lenders, and commercial finance firms looking to replace slow, manual document checks with AI-driven processing. It explains how the system works in real lending flows, where it delivers the most value, what challenges teams face during setup, and how to roll it out as a production-ready system based on real-world experience.

Why Manual Document Verification Fails in Lending Operations

Speed, accuracy, and compliance are no longer differentiators; they are baseline expectations. Teams that still rely on manual document workflows are competing at a structural disadvantage. Here’s why:

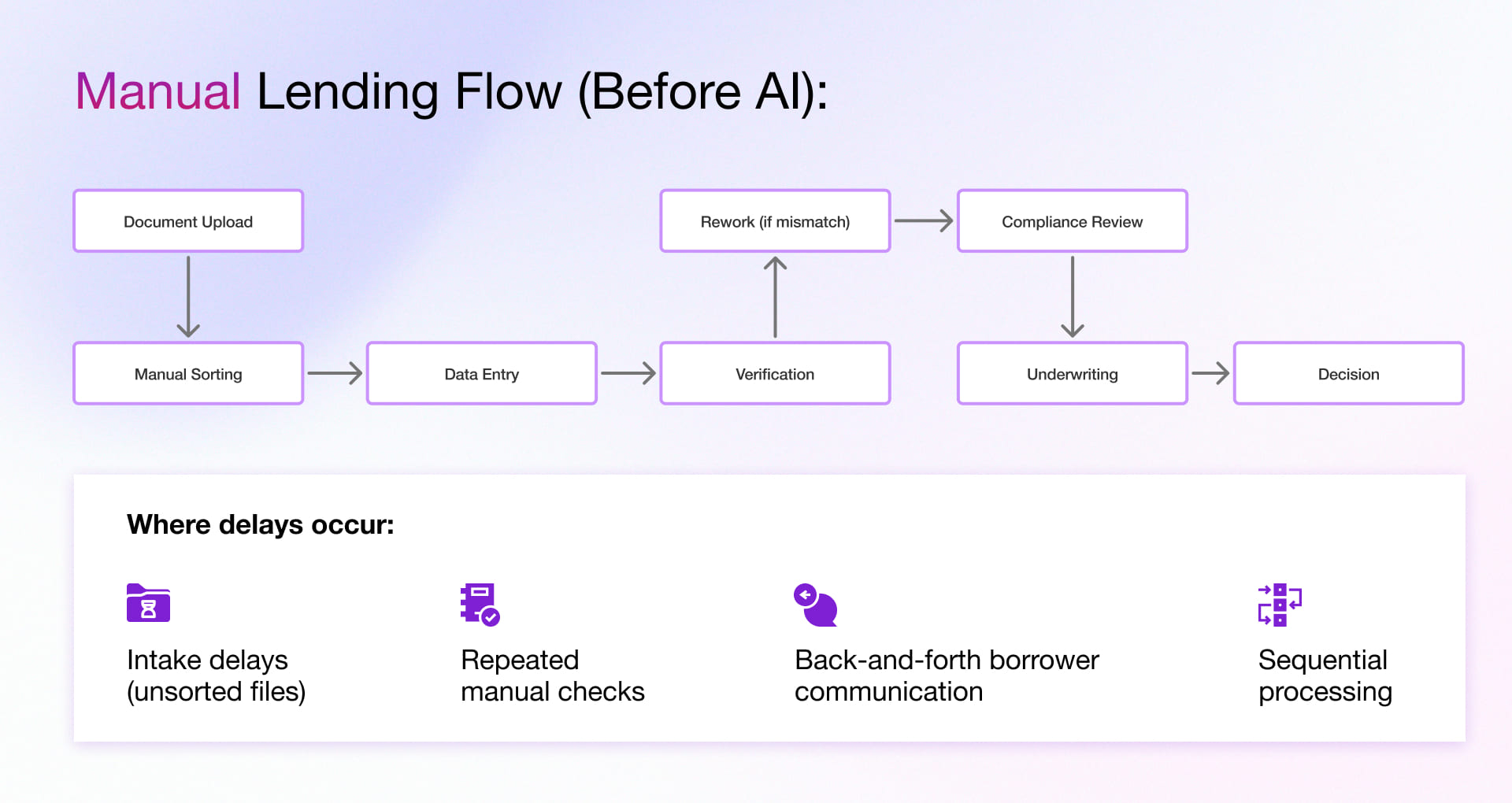

Manual Loan Document Review Slows Down Lending Operations

In a typical lending workflow, documents move sequentially across processors, underwriters, and compliance teams. Each handoff introduces delays. Each missing document restarts the cycle.

The impact is not operational; it is financial:

- Applications stay longer in pipeline → increasing cycle time

- Borrowers lose patience → reducing pull-through rates

- Teams spend more time per file → increasing cost per loan

- Underwriters receive incomplete files → lowering decision efficiency

As volumes increase, the system doesn’t scale. It slows down. This creates a hidden bottleneck where strong demand does not convert into funded loans.

Rising Borrower Expectations Are Pushing Lenders Toward Faster Approvals

Most applicants apply to more than one lender at the same time and go with whoever responds first. A 5-day wait that borrowers accepted five years ago now drives drop-offs. Slow document review does not just create an internal headache. It costs you to fund loans. Every extra day in the process gives the borrower more time to say yes to someone else. AI based document processing cuts that wait from days to hours.

Compliance Pressure Makes Document Accuracy Non-Negotiable

KYC and AML rules keep getting stricter, and regulators now examine how lenders handle documents in detail. Manual reviews increase risk, while teams cannot check thousands of documents with the same consistency under time pressure. AI-powered document automation runs the same checks on every file and logs every action. It reduces errors, improves consistency, and creates a clear audit trail for every decision.

How Intelligent Document Processing for Loans Works in Modern Lending Workflows

When borrowers submit loan documents, they come as mixed files, poor scans, and in different formats. Traditionally, teams spend hours just sorting, reading, and checking them. The use of AI in document processing changes that completely!

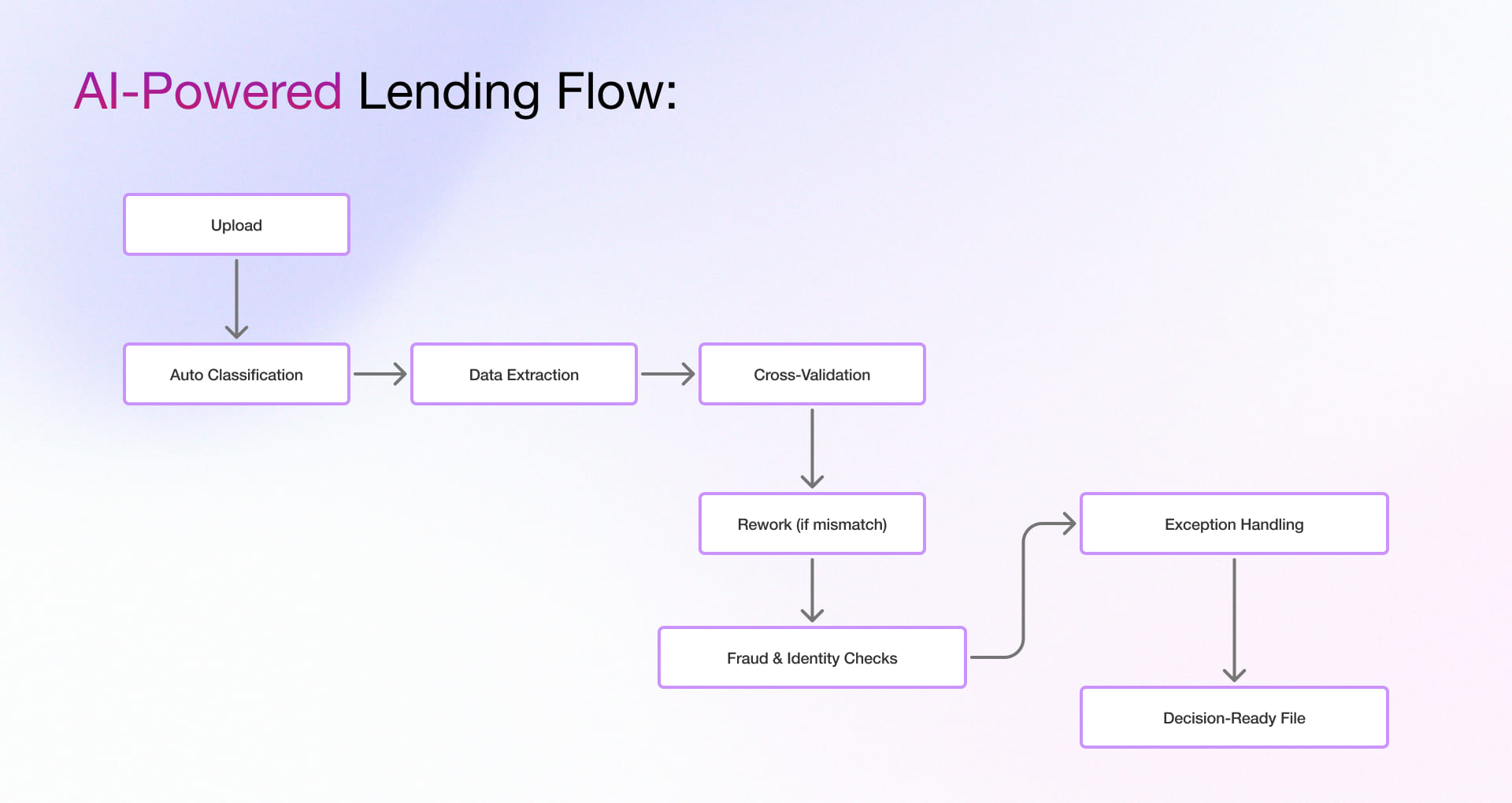

Intelligent document processing for loans is not a standalone technology. It is a coordinated pipeline of AI capabilities that handles intake, extraction, validation, and exception management in sequence.

How AI Powered Document Processing Works in Lending

Loan origination is already a multi-step process. Adding manual document handling makes it slower and error-prone. AI removes this friction by turning document processing into a parallel, automated pipeline:

Auto Classification & Routing

Auto Classification & Routing

AI instantly identifies documents (bank statements, ID proofs, income docs) and routes them to the right workflow.

No manual sorting. No delays at intake.

Smart Data Extraction

Using OCR + AI, the system pulls key data like income, names, balances, GST details, even from blurry or unstructured files.

No manual data entry.

Cross-Document Validation

AI checks everything together:

- Income vs bank statements

- Name consistency across docs

- Address and business details

Issues are flagged instantly

Identity & Fraud Checks

The system verifies:

- Face match & liveness

- ID authenticity (barcode, MRZ, tampering signals)

- Document forgery detection (edits, inconsistencies, overlays)

Ensures the borrower is genuine.

Exception Handling with AI

If something doesn’t match:

- AI flags the issue

- Explains the discrepancy

- Prepares a summary for underwriters

Teams review decisions, not documents.

Real-Time Borrower Requests

Missing something?

AI asks borrowers for exactly what’s needed, instantly.

Fewer follow-ups. Faster approvals.

Instead of:

- Sorting files

- Entering data

- Manually checking everything

Your team gets clean, verified, decision-ready applications. AI removes the busywork, so they focus only on real risk and decisions.

Looking to build a lending product from the ground up? See how we approached money lending app development, from architecture decisions to compliance-first design for founders building in regulated markets.

High-Impact Use Cases of AI-Powered Document Processing in Lending

AI-based document processing is not a single feature but a capability that compounds across every stage of the lending workflow. Here’s where document processing using AI moves the needle fastest for FinTech lenders and SME finance firms:

For SME Lenders

- Bank statement analysis for cash flow assessment

- GST and tax document validation

- Business identity and ownership verification

For Consumer Lenders

- Pay slip and income verification

- ID and address validation

- Bank statement parsing for eligibility checks

For Microfinance Lenders

- Mobile-first document capture

- Low-quality image processing

- ID validation and simplified risk scoring

For Commercial Finance Firms

- Financial statement extraction

- KYB and ownership structure validation

- Collateral and legal document analysis

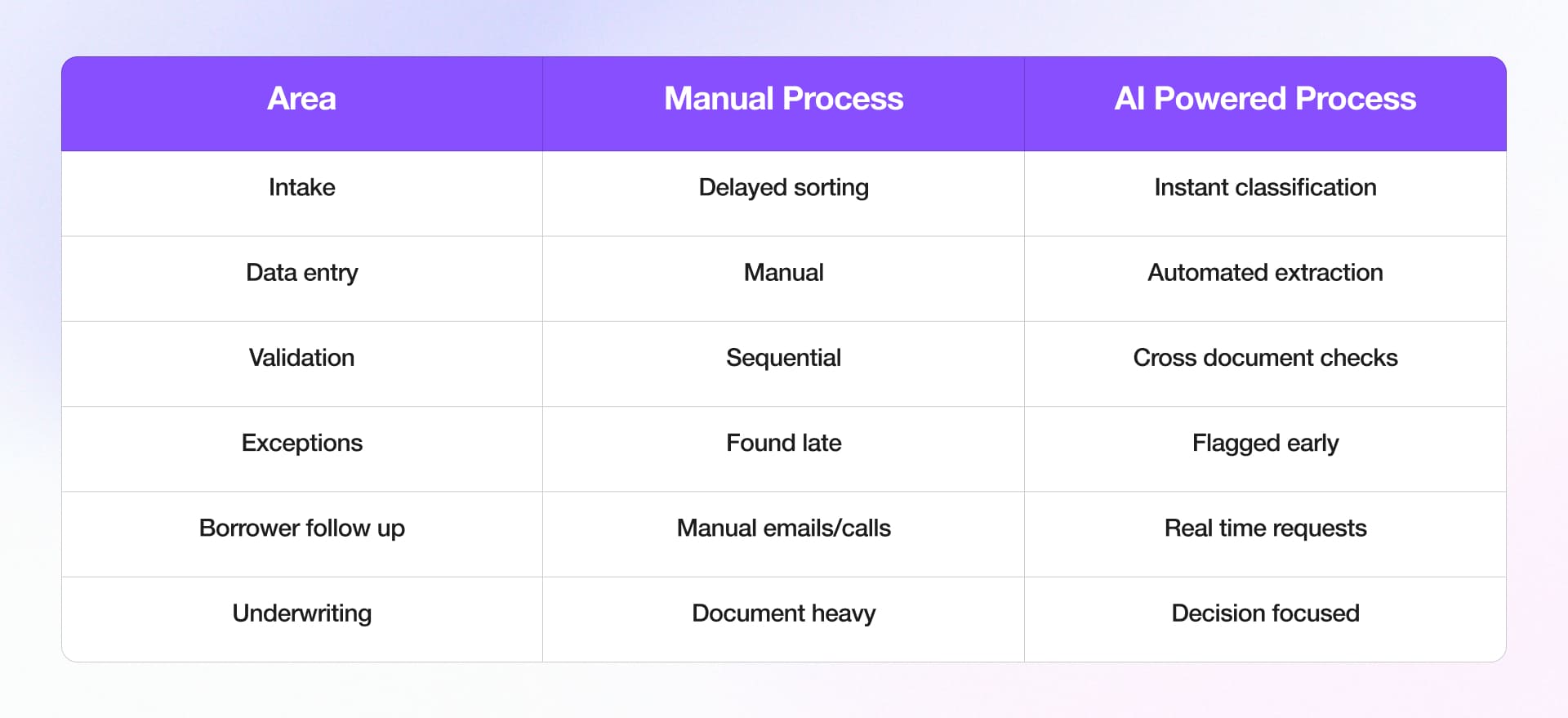

Key Benefits of AI-Based Document Processing in Lending Operations

AI document processing delivers measurable improvements across speed, cost, accuracy, and scalability. These gains show up directly in day-to-day lending operations.

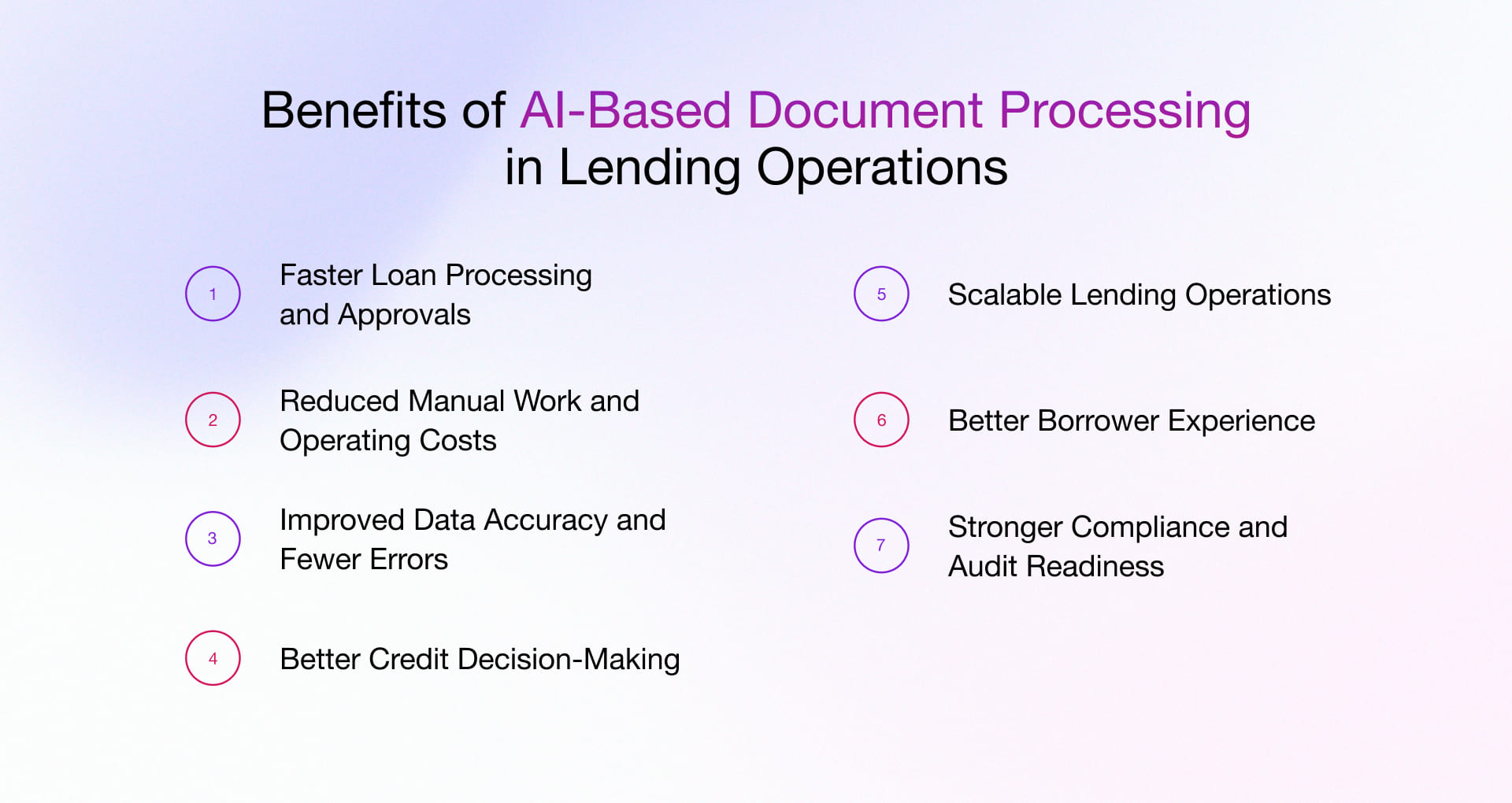

Faster Loan Processing and Approvals

AI automates document intake, extraction, and validation, reducing processing time from days to hours. Applications move forward instantly, even outside business hours.

Up to 60–70% faster turnaround time

Reduced Manual Work and Operating Costs

Teams spend less time on data entry, document sorting, and repetitive checks. The same team can handle higher volumes without increasing headcount.

30–70% reduction in cost per loan

Improved Data Accuracy and Fewer Errors

AI extracts and validates data across documents before it reaches underwriting. It flags inconsistencies early, reducing rework and improving data quality.

90%+ extraction accuracy with minimal re-verification

Better Credit Decision-Making

Underwriters receive clean, structured, and pre-validated data. They focus on risk assessment instead of reviewing documents.

Stronger decisions with up to 30% lower default rates

Scalable Lending Operations

AI removes the dependency between loan volume and team size. Lenders can handle spikes in applications without operational strain.

High-volume processing without proportional hiring

Stronger Compliance and Audit Readiness

Every step in the process is tracked and documented. AI ensures consistent validation and creates audit-ready records automatically.

Built-in compliance without added overhead

Better Borrower Experience

AI detects missing documents in real time and requests only what is needed. Borrowers get faster updates and fewer follow-ups.

Higher conversion rates and improved satisfaction

Using AI for document processing improves lending end-to-end. It enables faster decision-making, reduces costs, strengthens risk management, and supports scalable growth without operational friction.

Challenges in Implementing Document Processing Using AI in Lending

Fintech founders and commercial finance leaders have seen enough overpromised technology. So here, without glossing over complexity, are the real challenges in implementing document processing using AI and how to navigate them before they become problems.

Legacy System Integration

Your LOS, LMS, CRM, and DMS don’t automatically connect to new AI layers. Integration requires careful API design and data mapping. The right partner connects without requiring you to replace core systems. The wrong one will tell you to rebuild from scratch.

Regulators Expect Explainability

Every AI-driven step in a lending context must be traceable: what was reviewed, what was found, what action was triggered, and why. Audit trail design must be a first-class requirement, not something added before the regulatory inspection.

Generic OCR Fails in Production

General-purpose document tools are not built for lending complexity. Models must be trained on lending-specific document types and validation scenarios. Deploying generic AI for document processing in a commercial lending context is like using a kitchen knife for surgery.

Data Privacy and Model Governance

Lending documents contain the most sensitive financial data a person holds. Privacy frameworks, bias testing across borrower segments, and model performance monitoring must be built in from the start, not added under regulatory pressure after go-live.

Document Variability Across Markets

Lending documents vary widely across regions, languages, formats, and issuers. A model trained on clean, standardized documents will struggle with real-world inputs such as handwritten declarations, local-language tax filings, and low-quality scans. Domain-specific training is what makes AI document processing work in production, not just in demos.

What Lenders Must Get Right

AI based document processing fails when treated as a plug-and-play tool. Success depends on solving these challenges with the right architecture, domain expertise, and long-term model management. The partner who has never processed a real loan file in a real regulated market will find out what they don’t know at your expense. If you’re evaluating partners for AI or FinTech infrastructure more broadly, see what a specialized fintech software development company brings to these conversations versus a general-purpose software vendor.

How Rishabh Software Enables Document Processing with AI in Lending

There is no shortage of companies that will offer to build you a document processing system. The question is not whether they can build software. The question is whether they understand what happens when a merchant’s loan application hits an edge case that the demo never covered, and whether they have the domain depth to have anticipated it in the first place.

Rishabh Software has successfully completed 10+ engagements across geographies, regulated and emerging markets, large NBFCs, and early-stage fintechs. We’ve earned an understanding of lending that shows up in architectural decisions, not just delivery timelines.

Our AI and Machine Learning Development Services combine our lending tech proficiency with AI engineering to build document processing systems that eliminate manual bottlenecks, reduce review delays and help lending teams process applications faster without disrupting existing systems.

What “we care” looks like in a lending engagement

Production-Ready from Day One

We design systems for real document types, real borrower behavior, and real compliance requirements. Our solutions work in production, not just in demos.

Compliance Built in, from the Start

We design audit trails, explainability, and data governance into the system from day one. This ensures regulatory readiness without last-minute changes.

Integration Without Disruption

We connect to your existing LOS and lending systems. You don’t rebuild to use what we build. Zero rip-and-replace.

Lending Expertise

Our teams understand lending workflows, underwriting needs, and operational challenges. We design solutions that fit how lending teams actually work.

Transparent Execution

You know what we’re building, why, and what tradeoffs we’re making. No surprises in production.

A partner relationship, not a project

We stay accountable to your business outcomes. We focus on improving your lending performance, not just delivering a project.

What We Bring to the Table

- 10+ lending engagements across multiple geographies

- Experience across regulated and emerging markets

- End-to-end capabilities including IDP, OCR, LLMs, and workflow automation

See this in practice: our microfinance loan processing case study demonstrates how AI-based document processing reduced turnaround time and operating costs for a high-volume lending operation in an emerging market.

From Manual to Mobile: A Microloan Success Story

An Africa-based fintech company partnered with Rishabh Software to replace its slow, manual loan process with a fully digital mobile platform. The goal was simple: automate everything from identity verification to loan disbursement while keeping the experience smooth for both customers and banking partners.

The Challenge

The existing process was largely manual:

- Document validation was slow which delayed loan reviews.

- No integrated tools for risk scoring or credit assessment.

- Customer identity mismatches across different ID types made verification difficult.

- Poor integration with partner banking systems slowed disbursements.

The Solution

Rishabh Software rebuilt the loan process from the ground up using a modern mobile app backed by a robust automation engine:

- End-to-end automation from KYC to disbursement.

- Proprietary algorithms for real-time credit risk scoring and instant approval decisions.

- Automated document handling and identity verification to eliminate manual checks.

- Fraud detection API that monitors transactions and flags suspicious activity in real time.

- Loan eligibility calculator that factors in salary, liabilities, income, and years of service.

- Seamless integration with partner banks and credit bureaus for live fund transfers and reconciliation.

The Results

62% reduction in loan processing time

80% improvement in loan distribution and Tier 2 & 3 bank partnerships

50% savings in operational costs

Frequently Asked Questions

Q: Will my lending workflow benefit from AI driven document processing?

A: You are ready if you check multiple of these:

- OCR accuracy is below 90% in real cases

- Teams spend significant time on manual corrections

- Document volumes are increasing

- Multiple documents need cross-validation

- Borrower drop-offs are rising due to delays

The more conditions you meet, the stronger the case for AI adoption.

Q: What documents should lenders automate first ?

A: Start with high-volume, repetitive documents:

- Bank statements

- Pay slips

- Tax documents

- ID proofs

These drive the highest manual effort and fastest ROI when automated.

Q: What is the future of AI document processing in lending with generative AI and AI agents?

A: AI document processing is moving toward generative AI and AI agents. Modern systems already extract and validate data. The next generation can analyze multiple documents together, detect complex fraud patterns, summarize files for underwriters, and identify missing information early. This shifts document processing from a back-office task to a core part of credit decisioning. Lenders who invest in lending-specific AI architectures now will have a compounding advantage as generative capabilities mature over the next 12–24 months.

Q: How do AI agents improve document processing in lending compared to rule-based systems?

A: Rule-based systems rely on fixed formats and break when documents vary. AI agents handle different formats, learn from new cases, and analyze multiple documents together. They can detect inconsistencies across documents that rule-based systems miss.

Q: How does AI based document processing integrate with existing lending systems like LOS and CRM?

A: AI fits into your existing systems flawlessly. It connects with LOS, LMS, CRM, and DMS through APIs and event triggers. Documents come in, the system reads them, pulls the data, and sends clean, structured output back into your workflow. Your origination process continues to run as is. The key requirement is that integration is designed with your specific system architecture in mind.

Q: How long does it take to implement AI powered document processing in lending workflows?

A: A focused rollout usually takes about 8 to 14 weeks. Teams start with high-volume document types for one loan product. That phase covers model training, system connection, audit setup, and testing with real users.

Wider rollout takes longer. Expect 4 to 6 months when you add more products, regions, or document types. You still see value early. Each phase goes live as it’s ready. No need to wait for everything to finish.