In today’s fintech landscape, organizations have heavily relied on software systems, workflow tools, and integrated compliance solutions to manage customer due diligence processes. Yet the need for transformation remains. Making Generative AI for customer due diligence the next step in its evolution.

The growing importance of both domains is reflected in their market growth:

- Global due diligence services market, which is expected to grow from USD 8.4 billion in 2025 to USD 16.2 billion by 2034.

- The Generative AI market is projected to rise from USD 22.2 billion to USD 324.7 billion by 2033.

Together, these trends highlight a growing need for more intelligent due diligence capabilities. As organizations invest more in CDD services, Generative AI has the potential to make those processes faster, more accurate, and more efficient by helping compliance teams analyze information, uncover risks, and make informed decisions at scale.

Exploring gen AI for customer due diligence? Then stay until the end. This blog explores where Gen AI delivers the most value, how fintech companies can implement it, and the key metrics they can use to measure its impact.

Rethinking Customer Due Diligence Using Generative AI: From a Process-Centric to an Intelligence-Centric Function

From decision-makers to heads of regulatory departments, everyone thinks carefully before investing in new technologies like Generative AI for customer due diligence. The fear is valid. Every new technology comes with its own risks, implementation challenges, and the need to educate and train resources. But one thing is certain: the challenges fintech organizations are facing today, especially within customer due diligence workflows, are becoming increasingly difficult to manage with traditional approaches alone. Let’s see in detail.

The Structural Limitations of Process-Centric CDD

In a traditional CDD architecture, intelligence is generated downstream, and an analyst reviews outputs from individual data sources and synthesizes them manually. The process is sequential, siloed, and inherently reactive. Key structural constraints include:

- Document intake is unstructured: PDFs, scanned IDs, utility bills, and incorporation certificates arrive in formats that resist automated processing.

- Risk scoring is largely rules-based: Deterministic logic cannot adapt to unusual risk indicators without manual rule updates.

- Narrative generation: SARs, risk memos, and EDD summaries are created from scratch by analysts working against tight regulatory timelines.

- Ongoing monitoring operates on periodic cycles rather than continuous intelligence updates.

- Adverse media screening is keyword-based and source-limited, generating high false-positive rates that consume analyst time without improving risk signal.

The result is a function that is expensive to staff, slow to respond, difficult to audit, and unable to scale without proportional headcount growth.

What Intelligence-Centric CDD Looks Like (Customer Due Diligence Using Generative AI)

An intelligence-centric CDD function inverts this architecture. Rather than generating intelligence at the end of the process, it embeds intelligence generation into every stage using structured and unstructured data, across multiple sources, in near real-time. GenAI in customer due diligence is the enabling layer that makes this inversion feasible.

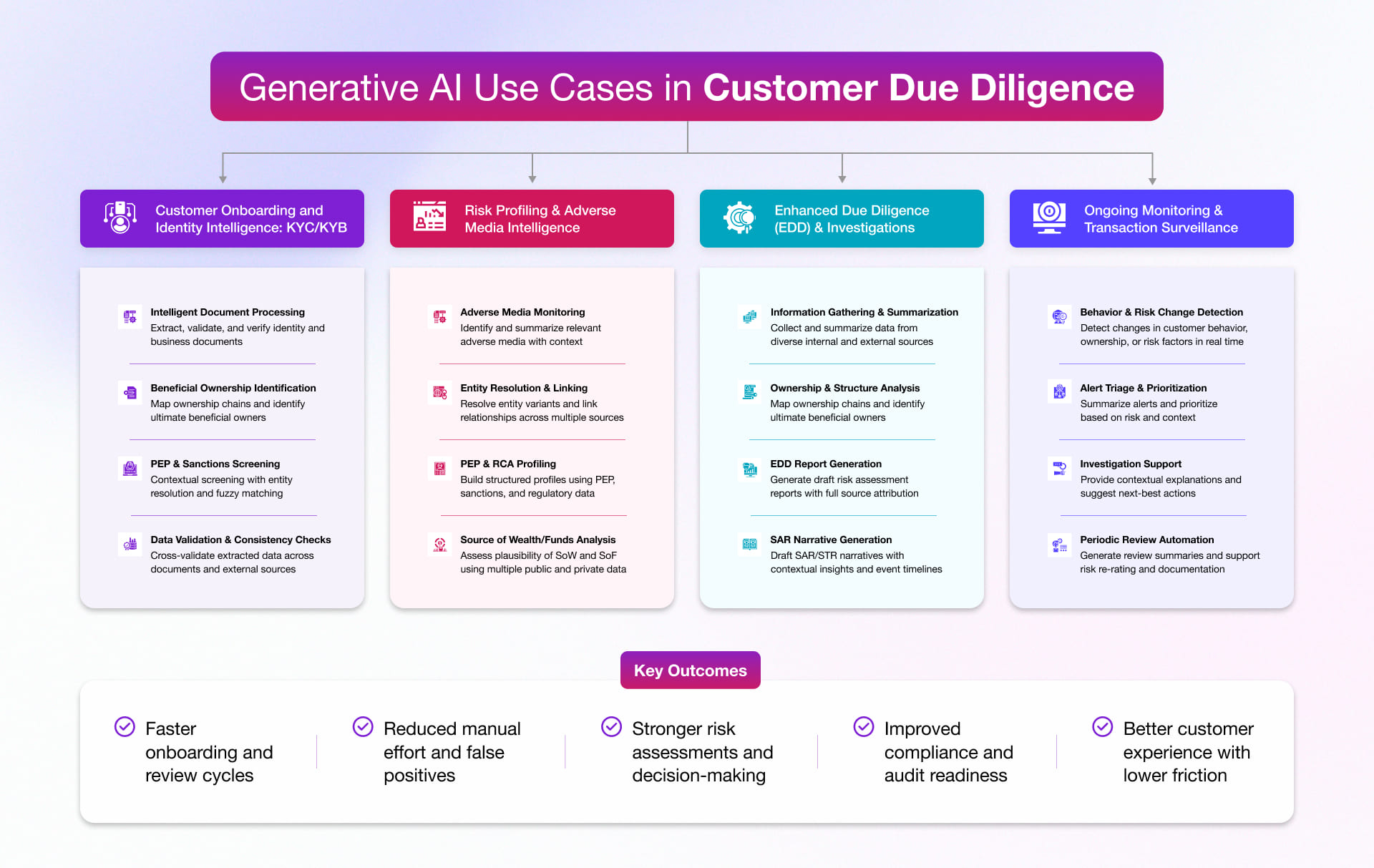

Where Generative AI Fits in the Customer Due Diligence Lifecycle with Use Cases

Generative AI in Customer Due Diligence can deliver value beyond basic automation when applied strategically and supported by domain experience. It adds value at four distinct stages of the CDD lifecycle, each with its own data inputs, intelligence requirements, and measurable outcomes.

1. Customer Onboarding and Identity Intelligence: KYC/KYB

Customer onboarding is the first stage where fintech firms verify individual customers and business entities as part of the broader due diligence process for onboarding. Customer due diligence using Generative AI can enhance this process through Intelligent Document Processing, where the system reads, extracts, validates, and summarizes information from passports, national IDs, proof of address, certificates of incorporation, director registers, shareholder documents, UBO declarations, and financial statements.

Real-world application:

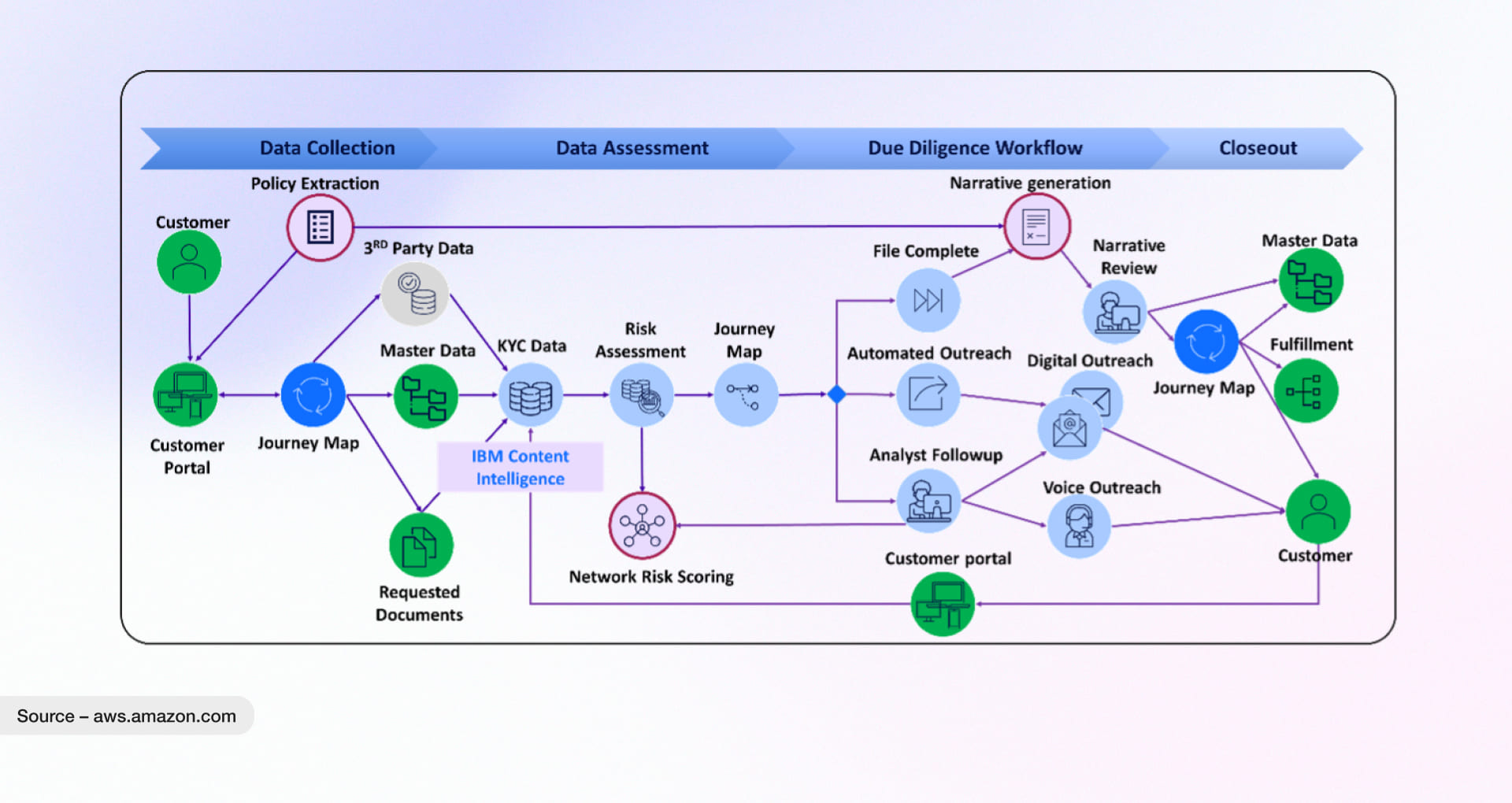

IBM Digital KYC on AWS uses Generative AI “digital workers” to support due diligence by reading, curating, and organizing policy and customer information for analysts. This helps reduce manual effort in document review and relationship mapping. Here is a flow of IBM digital KYC solution:

Sub-services enhanced by Gen AI:

- KYC document processing

- KYB document processing

- Identity verification support

- Business verification

- UBO identification and ownership mapping

- Document gap analysis

- Policy-based onboarding checks

- Automated audit trail generation

2. Risk Profiling and Adverse Media Intelligence

Risk profiling helps determine whether a customer presents low, medium, or high financial crime risk. In this area, the traditional approach and legacy systems are failing continuously. According to Retail Banker International, up to 95% of alerts generated by traditional AML systems turn out to be false positives.

Generative AI in customer due diligence improves this by analyzing information across sanctions lists, PEP databases, adverse media, regulatory records, corporate registries, and open-source data. No more manual efforts are needed for identification

Real-world application:

We have recently delivered an anti-money laundering solution to a leading US-based R&D company to accelerate the onboarding process, improve risk classification, and centralize account-opening management. This AML solution is backed by our AI and ML development services.

Sub-services enhanced by Gen AI in Customer Due Diligence:

- Customer risk scoring

- PEP screening

- Sanctions screening

- Adverse media screening

- Name matching and entity resolution

- High-risk jurisdiction checks

- Source-based risk summaries

- False positive reduction

- Customer risk narrative generation

3. Enhanced Due Diligence and SAR/STR Workflow Automation

EDD is the highest-cost, highest-stakes part of CDD. When a customer triggers an EDD obligation through PEP status, a high-risk FATF jurisdiction, a complex UBO structure, or a prior STR link, the compliance team must run a deep investigation

Generative AI in due diligence supports this stage by compiling information from multiple sources and converting it into structured investigation briefs, EDD reports, and SAR/STR narrative drafts. The need for this automation is growing as the global financial crime compliance market was valued at USD 26.52 billion in 2025 and is projected to reach USD 69.52 billion by 2034, growing at a CAGR of 11.40%.

Sub-services enhanced by Gen AI:

- Enhanced Due Diligence report generation

- Source of Wealth review

- Source of Funds review

- Beneficial ownership analysis

- Adverse media chronology

- High-risk customer review

- Case summary generation

- SAR narrative drafting

- STR narrative drafting

- Regulatory evidence compilation

4. Transaction Monitoring and Regulatory Reporting

Transaction monitoring is an ongoing CDD activity where customer behavior is reviewed after onboarding. With the global payments industry processing around 3.6 trillion transactions worldwide and financial institutions filing 4.7 million SARs in FY2024, monitoring and reporting have become highly complex.

Gen AI adds a contextual intelligence layer by reviewing whether a transaction is unusual for that specific customer based on their profile, history, business purpose, geography, and counterparties. It can also support alert summaries, investigation notes, and SAR/STR reporting drafts

- Behavioral pattern analysis: detecting structuring, smurfing, rapid movement of fund

- Network analysis and related-account detection: identifying undisclosed account relationships through payment counterparty patterns and device signals

- Cross-border transaction risk: assessing international transfers against FATF jurisdiction risk ratings and SWIFT correspondent banking relationship risk, with automated TBML (trade-based money laundering) indicator flagging

Sub-services enhanced by generative AI for customer due diligence’s monitoring process:

- Contextual alert triage

- Transaction behavior analysis

- Payment screening support

- Suspicious activity detection

- Cross-border transaction risk review

- Network and related-party analysis

- Alert narrative generation

- Investigator decision support

- Ongoing monitoring

- Perpetual KYC trigger-based review

- Regulatory reporting support

Implementation Roadmap for Gen AI in Customer Due Diligence

Here are the key steps FinTech organizations need to follow to implement generative AI in due diligence.

Step 1: Audit Your Current CDD Stack and Identify the Gaps

Before introducing Gen AI, map how your CDD function actually works. Most FinTechs find that customer data is fragmented across KYC platforms, transaction monitoring systems, spreadsheets, email threads, and case management tools.

At each stage, ask:

Where does the data come from? Where does it go? Where does a human need to intervene?

- Audit output: a ranked list of manual intervention points, monthly volume, and analyst-hours consumed. Also perform AI readiness assessment.

- Decision: which problem to solve first, and whether your data infrastructure is ready or needs fixing first.

Step 2: Fix the Data Foundation Before Deploying Gen AI

Gen AI can only work if the data it relies on is structured, accessible, and current. Before scaling any Gen AI in customer due diligence use case, FinTechs need an AI-ready data foundation that can deliver trusted context, enforce governance, and support reliable retrieval across systems.

- A unified CDD data layer: customer identity data, KYB documents, risk events, transaction data, and screening outcomes accessible from one structured platform.

- A document ingestion pipeline: passports, incorporation certificates, UBO declarations, utility bills, and other documents must be ingested, processed, and stored in retrievable formats.

- Live external intelligence APIs: sanctions lists, Companies House, GLEIF, adverse media, and other intelligence sources must be machine-readable and current.

Confused about where to start or how to manage complex data challenges? Partner with Rishabh Software, a leading data modernization services provider.

Step 3: Build the Intelligence Layer for Your Highest-Cost Problem

With the data foundation in place, start with the CDD workflow creating the highest manual effort, such as KYC reviews, KYB checks, adverse media screening, or EDD support.

A Gen AI intelligence layer can extract document data, compare it with customer profiles, flag gaps, summarize exceptions, and help analysts make faster decisions. For teams building this from scratch or modernizing an existing workflow, Rishabh Software’s Generative AI consulting and fintech software development services can support solution design, development, and integration.

Step 4: Deploy, Validate, Then Expand

Before scaling Gen AI in customer due diligence, validate it in a controlled environment. What you can do or process you can follow is:

- Start with shadow mode

- compare Gen AI outputs with analyst decisions,

- move to assisted mode once the results are reliable.

After validation, expand to EDD reviews, ongoing monitoring, SAR support, and regulatory reporting. Keep every output traceable, reviewable, and backed by approved data sources.

Measuring ROI of Generative AI in Customer Due Diligence

ROI measurement for Gen AI in CDD operates across three value dimensions: operational efficiency, risk quality improvement, and regulatory defensibility. These three dimensions have their own attributes to measure based on timeline, relevancy, and more. Things are mentioned below to see

| ROI Area | What to Measure | Why It Matters | Where to Track It |

| Onboarding efficiency | Time taken to complete KYC/KYB reviews | Shows whether Gen AI is reducing onboarding delays | KYC platform or onboarding dashboard |

| Analyst productivity | Time analysts spend on document checks, alert reviews, and EDD preparation | Shows whether analysts are spending less time on repetitive work | Case management system or workforce reports |

| Exception handling | Number of cases requiring manual review | Helps measure whether Gen AI is improving straight-through processing | CDD workflow dashboard |

| Screening quality | Number of irrelevant adverse media or transaction monitoring alerts | Shows whether Gen AI is reducing false positives and improving prioritization | Alert disposition logs |

| EDD efficiency | Time required to prepare EDD reports and risk summaries | Measures whether Gen AI is helping analysts prepare complex reviews faster | EDD case management system |

| SAR/STR support | Time required to prepare investigation summaries or draft narratives | Shows whether Gen AI is improving documentation speed and consistency | Compliance workflow system |

| Audit readiness | Availability of source-backed evidence, review history, and approval logs | Confirms whether Gen AI outputs are traceable and defensible | Audit logs, model governance records, and compliance reports |

How Rishabh Software Helps Build Gen AI-Powered CDD Solutions?

The right implementation partner matters as much as the technology architecture. Rishabh Software, a forward-thinking Gen AI solution provider, brings the combined strength of AI engineering and FinTech domain knowledge, and compliance-aware delivery to help build reliable CDD solutions. From RAG architecture and human-in-the-loop workflows to KYC/KYB integrations, model governance, audit trails, and build-vs-buy guidance, we help organizations design Gen AI systems that are scalable, explainable, and ready for regulated customer due diligence environments.

Frequently Asked Questions

Q: What Is Required to Implement Generative AI in Customer Due Diligence?

A: The first step is identifying where analysts spend the most time. For many FinTech organizations, that means reviewing KYC and KYB documents, conducting adverse media checks, preparing EDD reports, or investigating alerts. Once those bottlenecks are understood, Generative AI can be introduced to support data extraction, risk analysis, summarization, and documentation. Success depends less on the model itself and more on the quality of the data, workflows, and review processes surrounding it.

Q: Where Does Generative AI Add Value Across Different CDD Types?

A: Customer Due Diligence spans three regulatory tiers, each demanding different depth of intelligence:

- Simplified CDD (SDD): Applied to lower-risk customers (e.g., basic retail accounts). Focused on identity verification and basic source-of-funds.

Gen AI impact: automated document extraction, instant identity corroboration across registries. - Standard CDD: The baseline obligation for most FinTech customer relationships. Includes beneficial ownership mapping, adverse media screening, and PEP/sanctions checks.

Gen AI impact: multi-source synthesis, false-positive reduction, risk narrative generation. - Enhanced Due Diligence (EDD): Triggered by elevated risk indicators: high-risk geographies, complex ownership structures, PEP status, or unusual transaction patterns. Requires deep investigative analysis.

Gen AI impact: highest-value application — cross-source intelligence synthesis, SAR drafting, EDD report generation.

Q: How Do FinTech Organizations Measure the ROI of Generative AI in Customer Due Diligence?

A: The most common indicators are faster KYC and KYB onboarding, fewer false-positive alerts, reduced analyst workload, quicker EDD investigations, and improved audit readiness. If compliance teams can process more cases without increasing headcount while maintaining regulatory standards, Gen AI is delivering measurable ROI.