A borrower opens your app at 11:43 PM on a Tuesday. They need a $5,000 personal loan to cover an emergency. They’ve already been turned down by their bank, too slow, too much paperwork. So, they are shopping.

They apply with you. Then, while waiting, they open two other tabs.

What happens in the next four minutes determines whether you fund that loan or whether one of those other tabs does.

That four-minute window is not a UX problem. It’s not a marketing problem. It’s a loan origination system problem.

The lenders gaining market share have one thing in common: they have removed the operational bottlenecks that slow decisions down. McKinsey reports that leading banks using digital and automated lending processes have brought “time to yes” down to as little as five minutes (from days or weeks), while time to cash can be under 24 hours. The tools exist, the architecture is documented. The only question is whether your LOS is built to thrive beyond 2026 or whether it’s still a digital wrapper on a paper process.

This guide is your blueprint to build it right, the first time. You’ll walk away with the kind of clarity that usually only comes after you have already made the expensive mistakes.

What is a Modern Loan Origination System?

Application intake, identity verification, credit decisioning, underwriting, document management, compliance checks, loan funding, the LOS orchestrates all of it.

A legacy LOS is like a factory floor designed in the 1990s: assembly lines that can’t be reconfigured, machines that don’t talk to each other and supervisors who spend half their day on paperwork. It sure gets the job done but, slowly, expensively and with considerable human effort.

A digital loan origination system is more like a Tesla Gigafactory! Modular, automated, instrumented at every stage and designed to get faster as it learns. 3 things define it:

- Cloud-native

Elastic infrastructure that scales up when applications spike and scales down when they don’t. You only pay for what you use & not for capacity you might need someday. - API-first

Every component speaks a common language. This means swapping your KYC provider, adding an open banking integration & connecting to a new bureau takes just a few days, not quarters. - AI/ML-powered

Decisioning models that improve with every loan you make, not static scorecards that were calibrated in 2019 and are slowly deviating from reality.

Why Digital Lenders Need a Modern Loan Origination System (LOS) in 2026

Here’s a number that should make any lending operations leader uncomfortable:

- For loan applications, abandonment rates fall between 26% and 50% at most institutions, with some losing up to 75% of potential borrowers.

- Nearly half of all customers (48%) abandon because the process is too long or complicated.

- Mobile-unfriendly forms increase drop-off rates by up to 60%.

- The identity verification step alone can drive away 30–40% of applicants when document upload or KYC tools are clunky.

- Around 22% of borrowers aged 18–34 switch to a different lender due to poor clarity in the application process.

| Metric | Legacy LOS | Modern LOS |

| Approval Time | Days to weeks | Minutes to hours |

| Integration | Locked, proprietary | API-first, open ecosystem |

| Decisioning | Static scorecards | AI/ML, adaptive models |

| Scalability | On-premise, capacity-bound | Cloud-native, elastic |

| Compliance | Manual, retrospective | Automated, real-time audit trail |

| Cost Per Loan | High, scales linearly | Decreases with volume |

| Data Sources | Bureau only | Bureau + alternative + open banking |

The underlying dynamics have shifted in ways that make this more acute every year, not less.

Speed is now a product feature

When FinTechs like Blend and Upstart introduced near-instant decisions, they changed borrower expectations. In 2026, a same-day decision is no longer a competitive advantage. It’s the baseline!

Every manual step increases compliance risk

Untracked emails, off-system exceptions and undocumented decisions create audit gaps. Regulators now expect explainable decisions, documented workflows and complete audit trails. Legacy loan origination platforms make that difficult.

Alternative data has changed underwriting

While credit scores reflect past behavior, bank transactions, payroll data and open banking feeds provide a real-time view of a borrower’s financial health. But lenders can only use that advantage if their LOS can process the data.

The unit economics inversion

Legacy systems require more people as loan volumes grow. Modern loan origination platforms automate routine work which allows lenders to scale without increasing costs at the same pace.

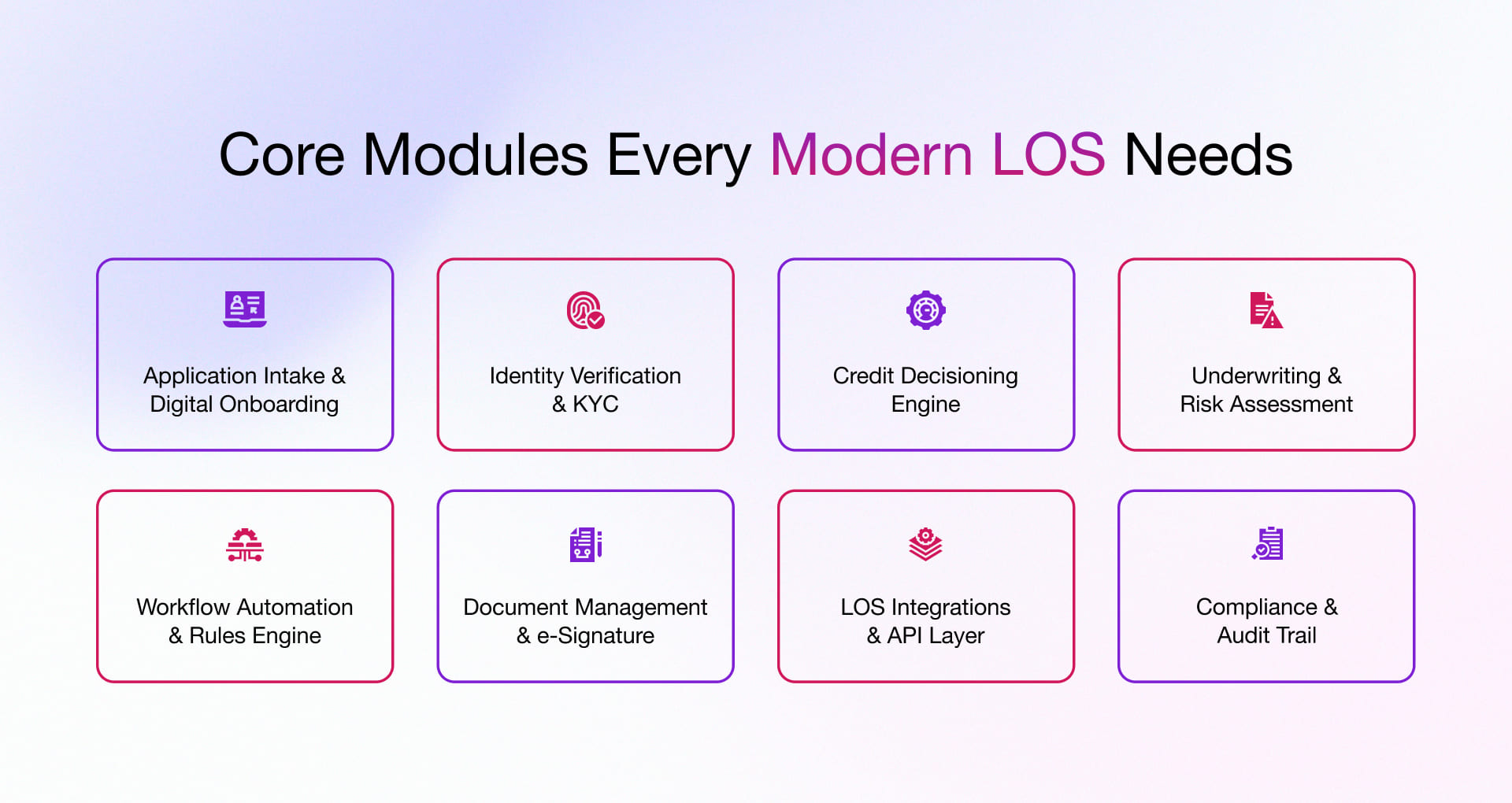

Core Components of a Scalable Loan Origination System Architecture

A modern LOS is not one system. It’s eight modules working as one with each performing a distinct job, each exposable as an API, each replaceable without taking down the others. Here’s the anatomy:

1. Application Intake & Digital Onboarding

Your intake module is your highest-leverage conversion point. A borrower who abandons the process costs you the same in marketing as one who completes but generates zero revenue.

Every extra field bleeds completion rate by 3 to 5%. The fix isn’t a shorter form but a smarter one. Open banking pre-fills income data, progressive disclosure shows only what’s needed, and real-time validation catches errors before submit.

With most borrowers applying on smartphones, mobile-first design directly impacts conversion rates. More than 70% of small personal loans are applied for and approved on smartphones, with funds often disbursed in under four minutes.

Building a borrower-facing loan app alongside your LOS? Here’s what a production-grade money lending app needs to get right, from feature architecture to security and compliance.

2. Identity Verification & KYC

It used to mean a loan officer photocopying a license. Now it means biometric liveness check, document scan, sanctions, and PEP lookup. All done in under two minutes without needing a human.

One thing lenders operating across borders consistently underestimate: a jurisdictional routing engine. KYC requirements vary by state, country, and regulatory regime. The rules in California differ from those in New York and both differ from requirements in Germany. One provider does not cover every market equally well.

3. Credit Decisioning Engine (AI/ML)

Legacy systems answer “will this borrower repay?” using a rulebook someone wrote years ago. Blunt then, blunter now.

A real decisioning engine treats credit as a prediction problem. It pulls in bureau data, bank transactions, payroll feeds, rental history, alternative signals. It delivers a repayment probability, not a yes or no, with the factors behind that probability laid out clearly enough to satisfy adverse action requirements.

4. Underwriting & Risk Assessment

Some loans should not get an automated decision. Complex files, edge cases & high-value deals need a human brain. The module’s job is making sure that humans spend their time judging, not digging.

Old way: underwriters burn 40% of their productive day pulling data from five different systems and chasing missing documents.

New way: the full credit package is sitting in the queue before the underwriter opens the file. Risk summary already written, ratios calculated and documents extracted and organized. They read it, make a call, move on.

5. Workflow Automation & Rules Engine

Thirty things happen between “application received” and “decision sent.” Bureau reports ordered, KYC triggered, incomplete files flagged, edge cases routed, borrowers kept in the loop. On a legacy LOS, someone manages all of that manually. On a modern one, a workflow engine runs it on autopilot.

What matters most in the design: your ops team has to be able to change the logic themselves. New product launches, regulation updates, threshold changes. No engineering sprint, no waiting. BPMN-based visual editors make this possible without touching code.

Learn how AI-powered mortgage workflow automation is helping lenders streamline operations and improve turnaround times.

6. Document Management & e-Signature

Document collection kills loan timelines. The average mortgage file needs 20+ documents. Chase those by email and your cycle time is measured in days while competitors are counting in hours.

AI extraction turns every upload into structured data. A pay stub becomes income fields. A bank statement becomes a cash flow profile. Discrepancies get flagged the moment they appear; not on day four when an underwriter finally gets to the file.

e-Signature closes it out. No wet signatures. No overnight couriers. No “just one last thing we need from you.”

7. LOS Integrations & API Layer

Your LOS performs at the level of its integrations. The ones that matter:

- Credit bureaus: Major national bureaus plus regional equivalents for international work

- Open banking: Primary account-linking and data aggregation providers for your target markets

- Employment and income: Leading employment verification and income data services

- Property valuation: Dominant property valuation and real estate data providers in your lending geographies

- Core banking and LMS: Your institution’s core banking system and loan management system

- Communications: SMS, email and in-app messaging for borrower updates

Build an abstraction layer between your LOS core and every vendor. Your system talks to the layer. The layer talks to vendors. One goes down or doubles its pricing, you swap it out. Your core never knows the difference.

8. Compliance & Audit Trail

A regulator asks why your system declined Application #47,821 six months ago. You pull up the full log in seconds, or you spend the next week reconstructing it from email threads. One of those conversations ends lending licenses.

Every action gets logged and locked:

- Which model produced which score?

- Which rule triggered which outcome?

- Which underwriter made which override?

Beyond the logs, modern platforms monitor decisions for bias patterns, automate HMDA and CRA filings and enforce data residency so borrower data stays inside the geographic boundaries regulations require.

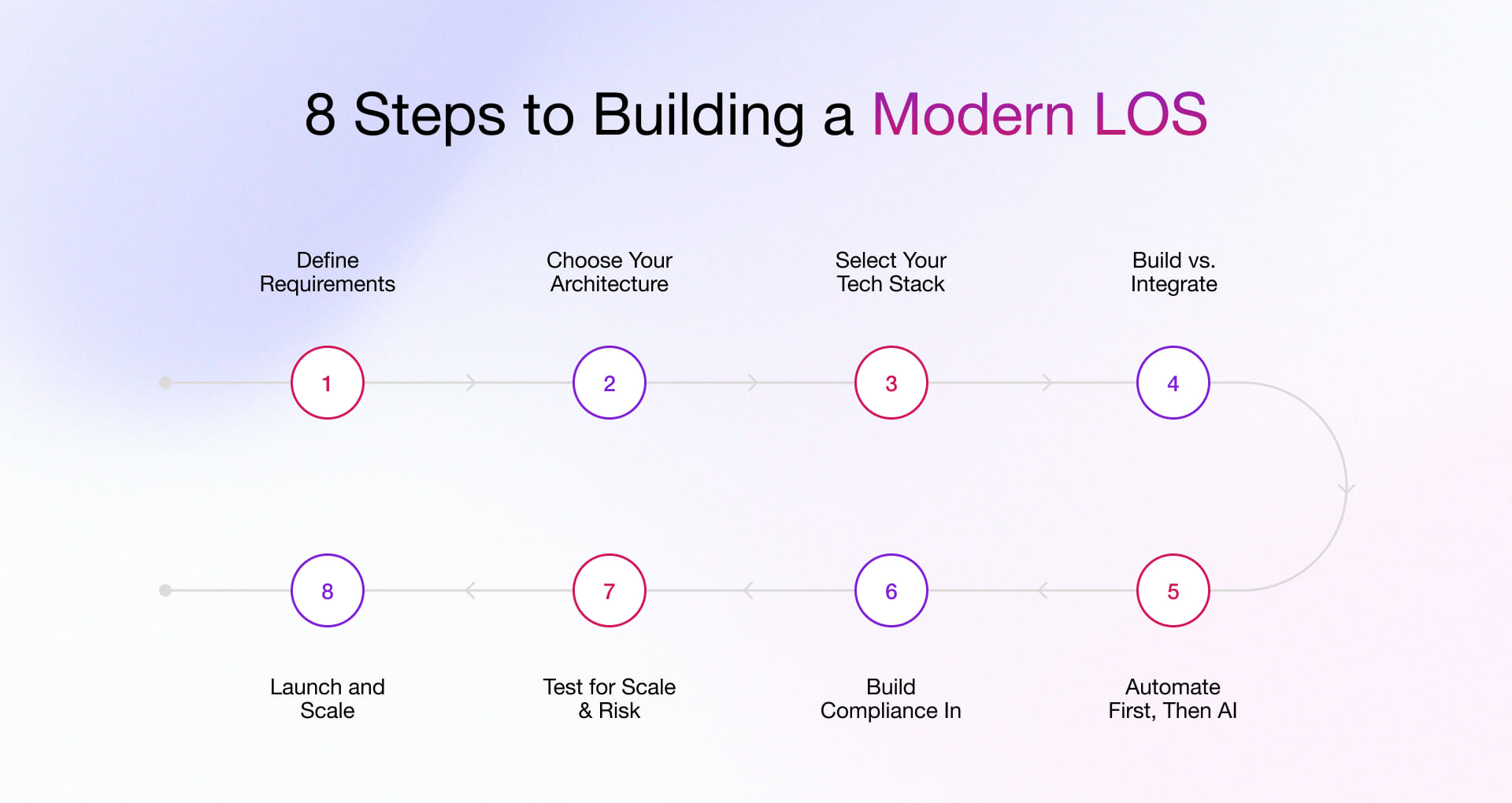

Step-by-Step: How to Build Your Loan Origination System Without Technical Debt

There’s no single blueprint for building a digital loan origination solution. The right approach depends on your products, borrowers, compliance requirements and growth plans. But the loan origination process steps below remain largely the same regardless of lender size or loan type.

Step 1: Define the Requirements

The most expensive mistake in LOS development is starting with technology and working backward to requirements. Do it the other way. Map every loan product you intend to originate. Document the borrower journey for each. Identify the regulatory frameworks that apply in every geography you operate. Define your data sources. Specify your decision logic. Draw the workflow – every step, every branch, every exception path.

Step 2: Choose Your Architecture

Three patterns to evaluate:

- Monolithic: One codebase, one deployment. Fast to build, harder to scale and change.

- Microservices: Independent services that scale and deploy separately. Highly scalable but operationally complex.

- Modular monolith: Clear module boundaries with a single deployment. A practical choice for many lenders because it balances flexibility with operational simplicity.

Pair your architecture with a cloud-native deployment strategy. Container orchestration platforms like Kubernetes help individual services scale automatically during traffic spikes.

Step 3: Select Your Tech Stack

Common choices for a modern LOS include:

- Frontend: React or Next.js

- Backend APIs: Node.js (with NestJS) or Go

- Workflow orchestration: Temporal.io or Camunda

- Database: PostgreSQL; Snowflake or Databricks for analytics

- Message broker: Apache Kafka or AWS SQS/SNS

- Cloud: AWS or Azure

- Infrastructure: Terraform

- Decisioning & ML/AI: Python (with FastAPI) + scikit-learn, TensorFlow/PyTorch

- API-First & Composable Architecture: Modular, open APIs for seamless integration with credit bureaus, fraud tools, e-sign (DocuSign) and core banking systems

- Observability: Prometheus + Grafana, Datadog, or OpenTelemetry

Step 4: Build Core vs. Integrate Commodity

Not everything needs to be built from scratch. Build what creates competitive advantage, such as your credit decisioning engine and underwriting models.

The question to ask for each module: is this a source of competitive differentiation, or is it a solved problem? Your credit decisioning engine – how you score borrowers, which data signals you weight, how your models are trained is likely proprietary IP. Build it.

Your KYC flow, your e-signature experience, your bureau integrations. These are commodity functions that third-party specialists have already solved better than you will on a first build. Integrate proven third-party solutions for functions like KYC, e-signatures and bureau connectivity.

Step 5: Implement Automation and AI in the Right Order

Start with the automation that has the highest ROI and lowest risk: automated bureau ordering, automated document extraction, automated income calculation and straight-through processing for clean, in-policy applications. Done well, this automates 60-80% of your application volume with minimal model risk.

Then build AI loan origination on top of that automation foundation. Start with a logistic regression baseline: interpretable, regulatorily defensible, a good benchmark. As your loan volume grows and your training data deepens, graduate to gradient boosted models. Once the automation foundation is in place, introduce AI models.

Read our blog on generative AI in fintech to see how financial institutions are applying AI across the loan origination lifecycle.

Step 6: Build Compliance In, Not On

Security and compliance built into architecture cost roughly one-third of what compliance retrofitted to an existing system costs. That ratio gets worse the longer you wait.

Non-negotiables from day one:

TLS encryption in transit, AES-256 at rest, field-level encryption for PII

- Role-based access with MFA enforcement and principle of least privilege

- Disparate impact testing integrated directly into the decisioning pipeline

- Geographic data routing rules enforced at the infrastructure layer

- Immutable audit logging for every system action

And build a regulatory change management process before you need it. Lending regulations change: federal guidelines, state-level updates, new AI explainability requirements. The lenders who manage this well have a rules engine that operations can configure without a code deployment. The ones who don’t are filing emergency engineering tickets every time a regulation changes.

Step 7: Test Like Your License Depends On It

An LOS handles financial transactions and sensitive borrower data. Testing needs to reflect that.

- Unit and integration testing

- Load testing at peak volume scenarios

- Parallel runs alongside existing systems

- User acceptance testing with operations teams

- Legal review of lending logic and adverse action notices

Step 8: Launch Small, Scale Eventually

Avoid moving all loan volume to the new LOS on day one. Pick a limited product type, a defined borrower segment, a controlled channel. Instrument everything. Let the monitoring tell you what to fix. Then expand. The lenders who do this well treat their LOS launch like a product launch, not an IT project. There’s a go-live owner, a rollback plan, a defined set of metrics that must hit targets before expansion and a war room for the first 72 hours.

The Decision You’re Really Making

Here’s the thing nobody says plainly: not deciding is a decision.

A legacy LOS doesn’t stay in the same place relative to the market. It falls further behind. Every month that passes, borrower expectations move up, competitors improve their automation and your manual processes accumulate more technical and regulatory debt.

The lenders who built modern origination infrastructure in 2022 and 2023 didn’t do it because they had budget to spare. They did it because they understood that the lending market was bifurcating into lenders who can operate at digital speed and cost, and lenders who can’t. And they decided they weren’t going to be the second kind.

Building a digital loan origination solution is one thing. Building one that works under real regulatory pressure, growing loan volumes, and complex integrations is another.

We Actually Built It – Real-World Loan Origination System Case Study Results

At Rishabh Software, we’ve delivered lending platforms across the US, Africa, and Southeast Asia, including mobile lending apps, asset-based lending platforms and end-to-end LOS solutions. We focus on building the right architecture for each lender and making compliance part of the platform from day one.

Case Study: Modernizing Asset-Based Lending for a US Lender

A US lender specializing in asset-based loans for small businesses was drowning in technical debt. Credit approvals were painfully manual, invoice reconciliation kept producing errors and managing multi-state compliance meant constant manual audits. The old system simply couldn’t handle growing loan volumes.

We modernized the asset-based lending system with scalable architecture, API-based integrations, automated compliance checks and real-time risk monitoring.

Results:

- 62% faster credit assessments

- 99% fewer payment processing errors

- 75% shorter regulatory reporting cycles

- 52% fewer data discrepancies

Read the full case study on legacy asset-based lending system modernization to learn how we rebuilt the compliance layer, risk engine and reporting stack.

Ready to build or modernize your loan origination software? Explore our lending software development services or book a free LOS assessment. We’ll map your current setup and show exactly how to close the gap.

Frequently Asked Questions About Building a Digital Loan Origination System

Q. How Long Does LOS Implementation Take?

A. The implementation of a commercial loan origination solution typically takes 2–6 months. Custom builds run 12–24 months depending on scope. Hybrid approaches land in the 6–12 month range. Integration work involving bureau connections, KYC, open banking and compliance readiness are reliably the longest poles in the tent.

Q. What are the Most Important Integrations For a Modern LOS?

A. In rough order of impact: credit bureaus, open banking and bank account data, employment and income verification, KYC and identity verification, e-signature, and core banking or LMS for loan servicing handoff.

Q. What are the Most Common Mistakes When Building a Loan Origination Software?

A. The most common mistakes happen during planning, architecture, and rollout.

- Teams pick the tech stack first and map requirements later. This always leads to rebuilding modules.

- Builders waste engineering hours on KYC, e-signatures, and bureau connections. Buy these. Build your automated loan decisioning engine instead.

- Compliance gets added at the end. Audit trails and data residency controls need to be architecture decisions made on day one.

- Lenders go live at full volume immediately. Start with one product, fix what breaks, then scale.

Q. How Do You Migrate from a Legacy LOS Without Downtime?

A. A phased migration helps reduce risk and avoid service disruptions.

- Run both systems in parallel. Move one loan product to the new LOS and leave everything else untouched.

- Connect your integrations before moving any loan volume. Bureau connections, KYC and core banking failures mid-migration are what blow up timelines.

- Treat data migration as a separate project. Map loan records, borrower history and documents cleanly before moving anything.

- Give yourself three to six months. Teams that rush it into six weeks spend the next six months fixing mistakes.

Q. What Does it Take to Build a Loan Origination System Software for Cross-border Lending?

A. Cross-border lending requires a platform built for regulatory and operational complexity.

- Build a jurisdictional routing engine. KYC rules, data residency laws, and lending regulations differ by country. Manual management breaks at scale.

- Build a decisioning engine that handles variable data inputs. Some markets have bureau data. Others rely entirely on bank transactions. Your model needs to handle both.

- Build local banking infrastructure into the core. Payment rails, disbursement methods, and repayment collection need to feel native to each market.

- Treat each new market as a configuration on your existing platform. Not a full rebuild every time.