The global digital lending market hit $5.58 billion in 2019. By 2027, it’s projected to reach $20.31 billion, a 16.7% CAGR that doesn’t slow down for anyone who isn’t ready.

The gap between ready and left behind is already visible in the data: only 27% of banks are actually prepared for what’s coming. The rest are watching AI-first institutions cut costs by 20% to 25% and grow revenue by 10–20%, wondering where they fell behind.

Digital-first lending isn’t a competitive edge anymore; it’s the baseline. This blog will help you understand what is a digital lending platform, the advantages of digital lending for both institutions and borrowers, and the moves financial institutions need to make right now to stay relevant in 2026.

Digital-First Lending: What the New Standard Actually Means for Lenders in 2026

Digital-first does not mean having a mobile app or accepting online applications. Putting a paper-based process on a screen is just digitization, and that is not the same thing.

Giving a horse a GPS tracker won’t turn it into a car. The form changes but the fundamental capability remains the same. A truly digital-first lending experience is built from the ground up around speed, real-time intelligence and personalization. It is not a legacy workflow with a digital layer added on top.

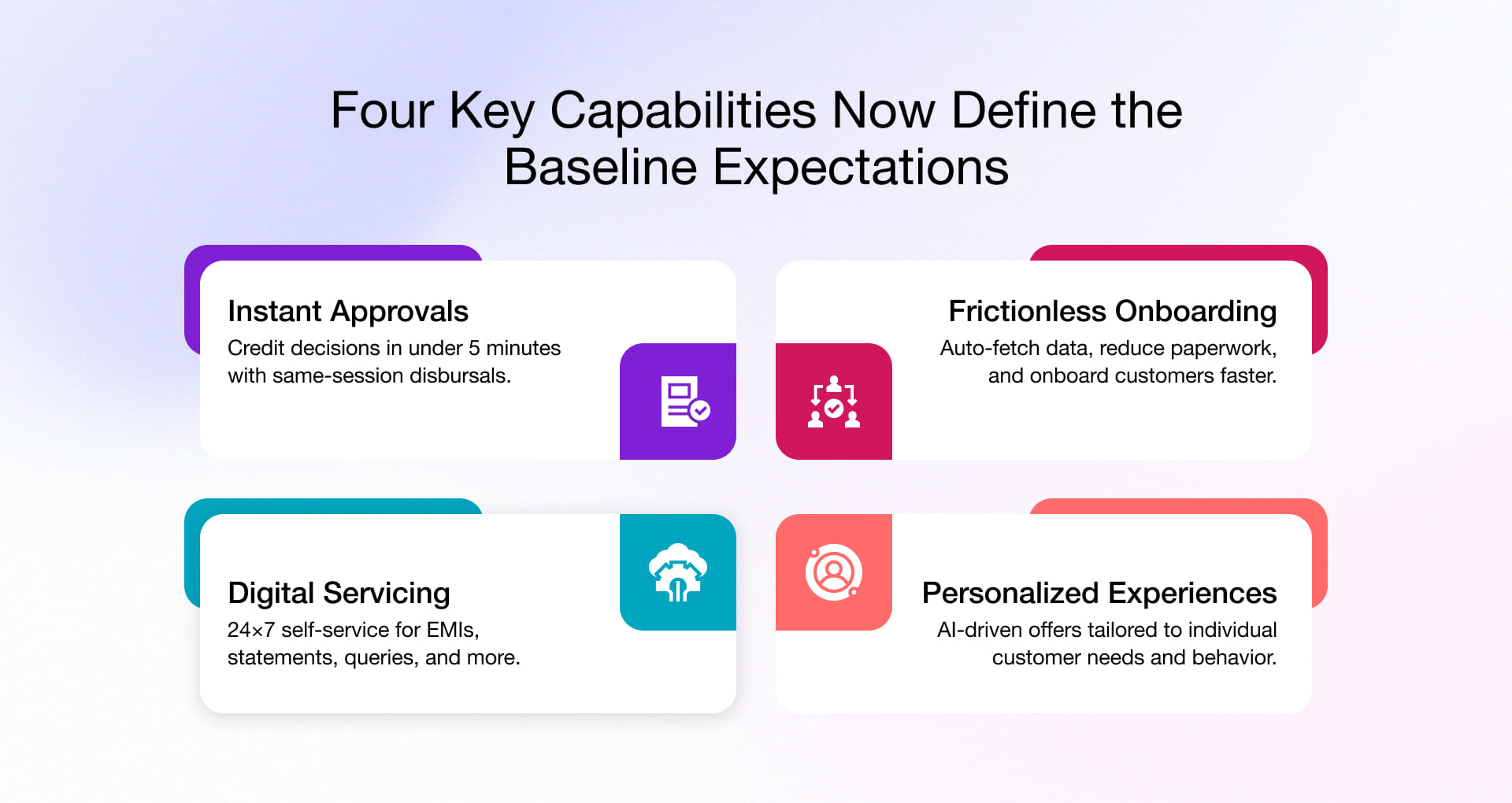

4 Must-Have Capabilities for Modern Lending Platforms:

1. Instant Approvals

Not “fast.” Instant. Leading platforms deliver credit decisions in under 5 minutes for pre-qualified borrowers. Same-session disbursals are the industry standard for digital consumer lending for top players. Any institution positioning same-day approval as a headline achievement is already behind the benchmark.

Rishabh Software modernized a legacy asset-based lending platform for SMB financing to accelerate their credit assessments and improve efficiency through automated lending workflows. Explore the case study: Legacy Asset Based Lending System Modernization for SMBs

2. Frictionless Onboarding

Every field a borrower fills in that a system could also pre-populate is nothing but friction. Every document manually uploaded that could be fetched via API consent is also friction. Every step completed on one device that does not carry over to another is friction. Frictionless onboarding means the borrower does less work because the platform does more. It automatically pulls verified identity, banking, income, and financial data through secure, consent-based integrations to reduce paperwork and speed up onboarding for borrowers.

See how Rishabh Software automated KYC, document verification, and loan onboarding for an Africa-based microfinance platform.

3. Digital Servicing

The loan relationship does not end at disbursal. It continues through every EMI, statement request, prepayment inquiry, and restructuring conversation. Digital-first institutions deliver these through self-service portals and intelligent virtual assistants, available at 2 AM on a Sunday, with full account context and without a call center queue.

4. Personalized Financial Experiences

A freelance designer and a manufacturing business owner may both need credit, but their borrowing needs, repayment capacity, and financial behavior are completely different. They need completely different amounts, tenures, and repayment structures.

A one-size-fits-all platform that offers them the same product is not serving either of them well. Digital-first platforms know the difference. They use behavioral data and AI models to build the offer around the individual with the right amount, tenure, and repayment rhythm, and deliver it before the borrower has already opened 4 tabs and filled out 3 competitor applications.

Why Banks and NBFCs Are Investing in Digital Lending Transformation

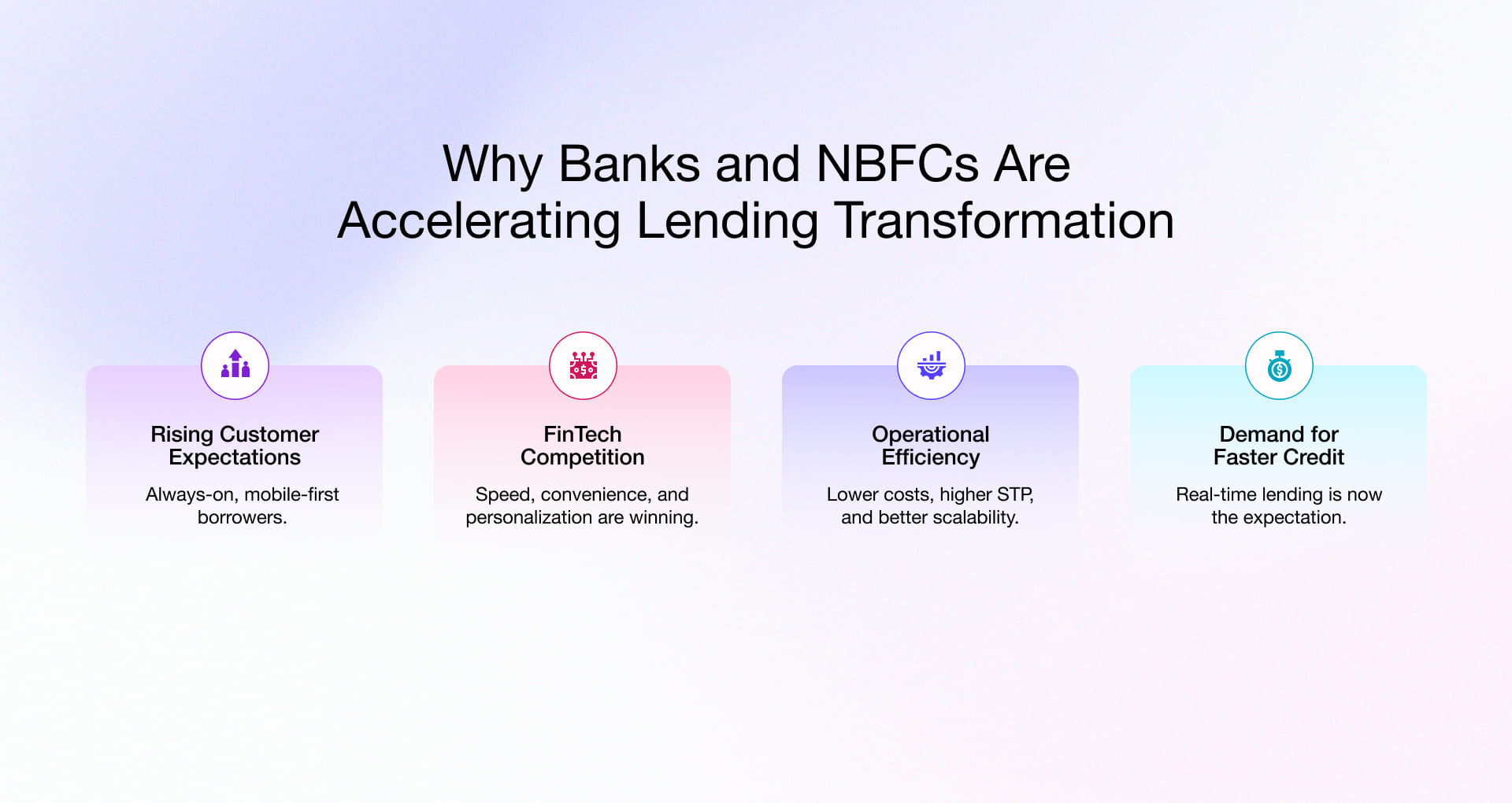

The urgency is arriving from multiple directions simultaneously. Understanding what is actually driving this digital transformation separates financial institutions genuinely modernizing from those running digital projects as brand window dressing.

Changing Customer Expectations: The Always-On, Mobile-First Borrower

The behavioral baseline has shifted permanently. The generation entering peak borrowing years today has never known a world without instant everything. Food delivered in 10 minutes. Flights booked in 90 seconds. Money is transferred instantly via real-time digital transaction networks. When that person sits down to apply for a business loan and hits a 72-hour wait for document verification, they do not adjust their expectations. They find a lender who matches them.

The demands are very specific:

- Instant experiences in terms of decisions, confirmations, and status updates in real time instead of business days

- Mobile accessibility with full-feature application, tracking and loan management from a phone

- Transparency with real-time visibility into application status, underwriting criteria, and decision rationale

- Self-service capabilities to manage the entire loan lifecycle independently, without branch visits or call center waits

A recent study found that 73% of consumers would switch banks for a better digital experience. Speed and experience have overtaken rate as the primary selection criterion. That is a structural market shift, not a temporary trend.

Competitive Pressure from FinTechs: When Speed Becomes a Moat

Five years ago, the FinTech threat to traditional lenders was largely theoretical. Today, it is documented market share erosion. FinTechs built for lending from day one, with cloud-native architecture, API-first design, and product teams who think in customer journeys instead of internal approval chains. Three things create a lasting competitive advantage in credit:

- Speed creates the first impression and often determines whether the borrower goes elsewhere. A FinTech decisioning engine integrated directly with bureaus, bank statement analyzers, and fraud APIs returns an answer in minutes. A traditional process routing applications through underwriter queues returns an answer in 4 days. That gap is not primarily a technology gap but an architecture glitch.

- Convenience reduces the cognitive load of borrowing to near zero. Pre-approved offers, single-tap acceptance, auto-debit setup in the same session and zero physical touchpoints. The best FinTech digital lending products remove every obstacle between the borrower’s intent and the funds arriving in their account.

- Personalization converts casual applicants into loyal customers. FinTechs price risk at the individual level, construct offers around demonstrated repayment capacity, and time outreach to behavioral triggers. Traditional lenders serve segments while FinTechs serve individuals, and the difference shows up in both conversion rates and portfolio quality. Banks and NBFCs can close this gap but with structural re-platforming.

Explore how Rishabh Software’s FinTech engineering services help banks and NBFCs modernize lending ecosystems for speed, scale and smarter decisioning.

Operational Efficiency: The Internal Cost Case

Beyond the competitive threat, the efficiency case for digital transformation stands entirely on its own. Manual lending operations scale linearly and expensively. Document handling, physical KYC verification, underwriter review queues, manual bureau pulls, and paper sanction generation each add cost per loan that does not shrink as volume grows.

McKinsey’s Global Banking Annual Review 2025 indicates that AI implementation across banking can deliver gross cost reductions of up to 70% in certain cost categories with a net 15–20% reduction in banks’ aggregate cost base. For an institution processing 40,000 loans per month, that cost differential is not a rounding error but a margin transformation.

Digital lending solutions enable straight-through processing (STP), where a loan moves from application to disbursal without a human touchpoint for standard cases. Every percentage point increase in STP rate reduces cost per loan and reduces processing time simultaneously. The platform processes the 10,000th loan with the same infrastructure as the first. That is not possible with a manual operations model.

Demand for Faster Credit Access: Real-Time Lending is Now the Expectation

The nature of credit demand has also changed. Borrowers increasingly need credit at moments of immediate intent rather than through a planned, scheduled process.

An MSME owner who spots a bulk purchase opportunity on a Tuesday afternoon cannot wait until Thursday for a decision on working capital. A salaried professional facing a medical emergency cannot navigate a week-long personal loan process. A first-time borrower exploring credit for a business idea will not persevere through a documentation-heavy, branch-dependent origination workflow.

Real-time lending infrastructure, built on automated underwriting and instant bureau integration, efficiently serves these emergencies. It converts credit demand at the point of need rather than losing it to informal lenders, family borrowing, or better-equipped competitors.

Key Lending Use Cases Benefiting from Digital-First Platforms

Digital-first loan platforms are transforming how financial institutions manage MSME lending, personal loans, embedded finance, collections, and loan servicing. Some of the biggest benefits of digital lending include faster approvals, reduced operational costs, wider credit access, better borrower experiences, and improved portfolio performance.

The table below highlights key digital lending platforms examples and the business impact they deliver across different lending use cases.

| Use Case | Buyer Pain | Platform Capability | Business Outcome |

| MSME Working Capital Lending | Slow underwriting and excessive documentation | GST, bank statement, bureau, and Account Aggregator integrations | Faster approvals and broader MSME reach |

| Personal Loans | High application drop-offs | Pre-filled journeys, instant KYC, automated eligibility checks | Better conversion rates |

| New-to-Credit Lending | Thin or no credit history | Alternative data analysis and AI-driven risk scoring | Inclusive lending with controlled risk |

| Embedded Lending | Limited customer reach | API-led partner integrations and OCEN-style lending flows | New acquisition channels |

| Loan Servicing | High call center dependency | Self-service portals, repayment automation, and chatbot support | Lower servicing costs |

| Collections & Early Warning | Delayed NPA detection | Behavioral analytics and predictive risk alerts | Lower delinquency rates |

The Impact of Digital Lending on Customer Experience and Risk Management

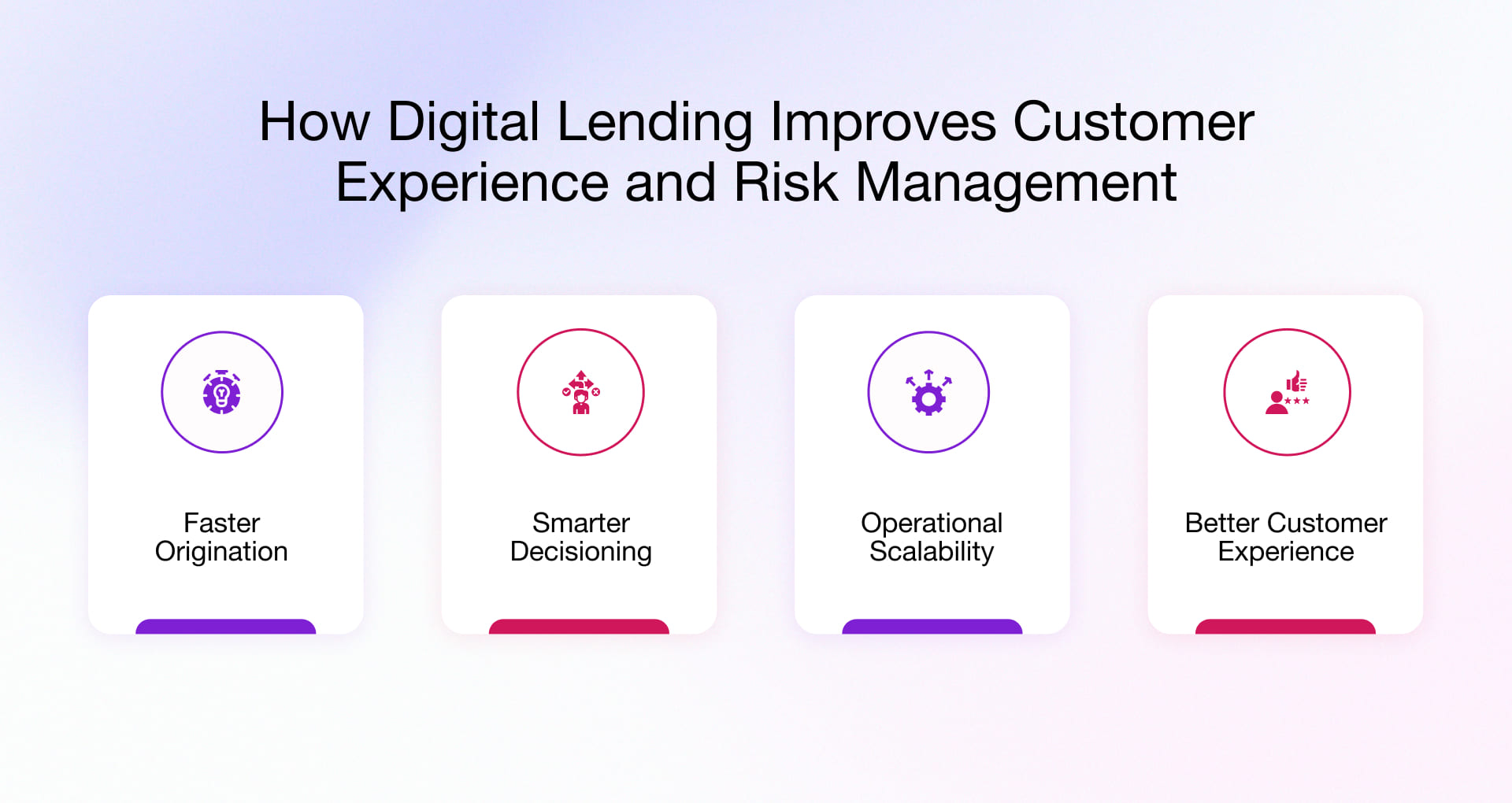

The payoff from digital lending transformation is measurable, documented, and arriving from multiple directions at once.

1. Faster Loan Origination and Approvals That Drive Conversion

Speed is a conversion metric, not just a customer satisfaction metric. When a borrower applies and waits five days, they do not wait patiently. They shop. And when a competitor says yes in an hour, the first lender does not get a second chance. Digital-first origination systems with automated document verification, real-time bureau integrations, and rules-based eligibility engines collapse loan origination timelines from weeks to hours. Leading NBFCs on fully digital stacks report average time-to-disbursal under 24 hours. That speed advantage compounds into measurable portfolio growth, without proportional increases in marketing spend.

2. Smarter Credit Decisioning Through Data and AI

Traditional credit scoring relies mainly on a borrower’s past credit history to predict future repayment behavior. It works reasonably well for borrowers with established credit histories.

AI-powered credit decisioning models completely change this equation. Modern digital lending fintech platforms ingest a richer signal set: bank statement cash flow patterns, tax filing consistency, eCommerce seller transaction history, telecom payment behavior, and cross-institution financial data via the Account Aggregator framework. The result is underwriting that is simultaneously more accurate for existing borrowers and more inclusive for new-to-credit segments.

McKinsey reports that banks using advanced credit-decisioning models have seen credit-loss rates decline by 20% to 40%, as the models more precisely estimate customers’ likelihood of default.

3. Operational Scalability and Cost Optimization

The traditional lending model has a ceiling. More loans mean more underwriters, more operations staff, and more branch infrastructure needed. That ceiling becomes a strategic liability as ambitions grow.

Digital-first platforms break that constraint. An AI-powered lending platform processes the 50,000th loan with the same infrastructure footprint as the 500th. When demand spikes during a festive season credit push, a new product launch, or a macroeconomic tailwind, the platform adapts to the volume. Manual operations would buckle under the same conditions.

4. Enhanced Customer Experience Across the Full Loan Lifecycle

The customer experience opportunity in a digital lending business extends far beyond a smooth application form. Lifecycle personalization means the platform works proactively and not reactively:

- A borrower who just closed a loan receives a relevant cross-sell offer within the optimal repayment gap window

- A borrower showing early behavioral stress signals receives proactive outreach before they miss an EMI, not after

- A customer who just received a salary increment receives a pre-approved top-up offer before they consider searching for one

This is not CRM. It is AI-driven engagement built on repayment behavior, product usage patterns, and life event signals, operating continuously across the borrower relationship. This lifecycle personalization drives measurably higher customer retention. McKinsey reports that one-to-one tailored engagement strategies can increase conversion and retention rates by 3 to 5 times. Retention is revenue that does not require re-acquisition spend.

How Embedded Finance and Multi-Channel Distribution Expand Lending Reach

Globally, about 1.7 billion adults remain unbanked. It is an untapped market worth trillions in credit demand, and the institutions that build the infrastructure to serve it today will own the market share that competitors spend years trying to claw back. Digital-first lending platforms help banks and NBFCs reach borrower segments that traditional branch-led models often miss. Lenders can serve MSMEs, gig workers, new-to-credit users, and underserved regions more efficiently through embedded finance partnerships, mobile-first experiences, API-led ecosystems, and alternative credit assessment models.

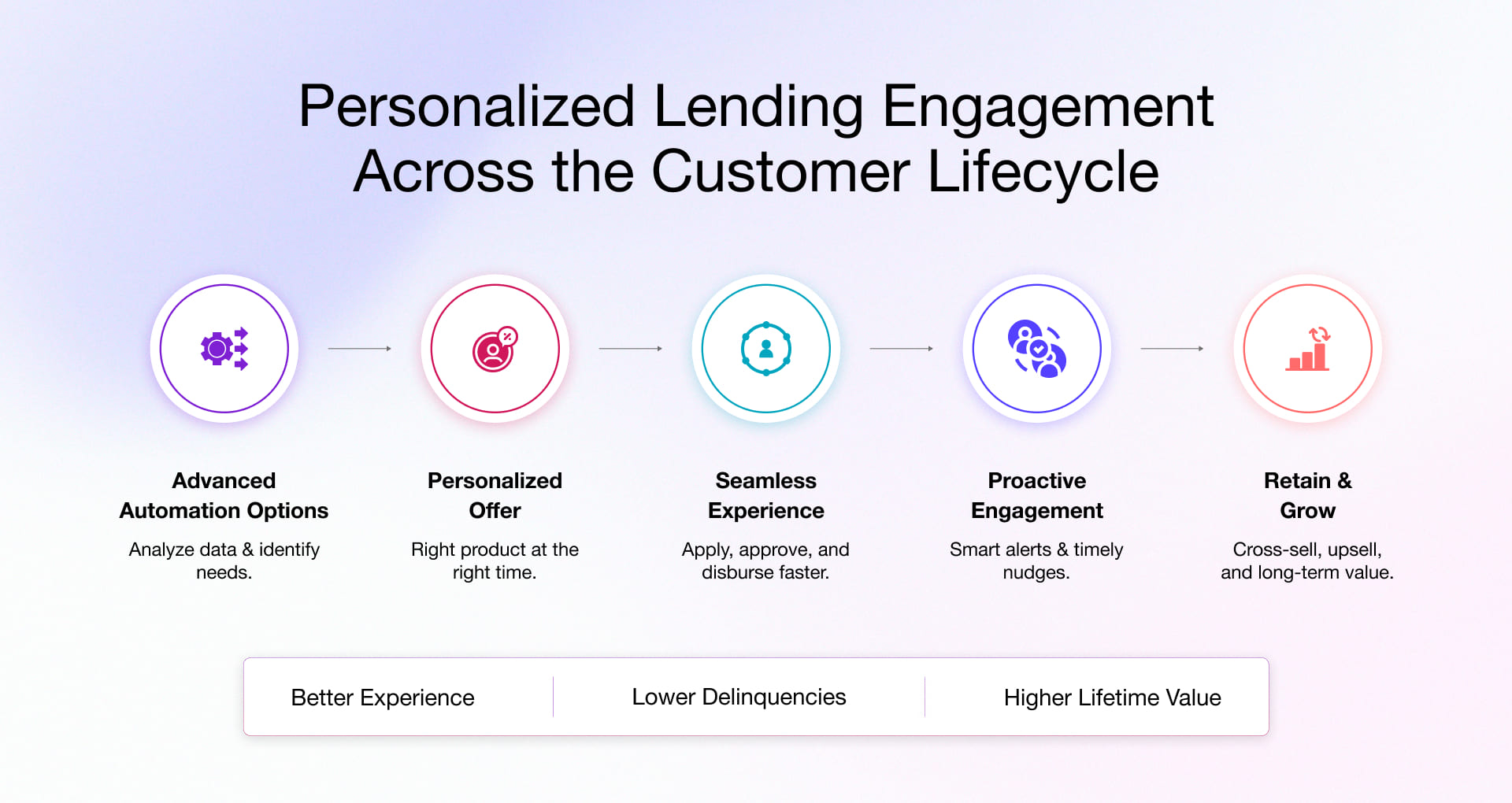

How Personalized Lending Drives Engagement Across the Customer Lifecycle

Modern borrowers expect faster, simpler, and more relevant lending experiences. Generic loan offers and mass outreach no longer drive engagement.

Digital-first lending platforms help banks and NBFCs deliver personalized experiences across the entire borrower journey. By using behavioral insights, repayment patterns, and AI-driven analytics, lenders can offer the right product at the right time through the right channel.

For example, a borrower with strong repayment behavior can receive a pre-approved top-up offer instantly. A small business with seasonal cash flow needs can get flexible working capital options tailored to its business cycle.

Personalization also improves every stage of lending:

- Pre-filled applications reduce friction

- Automated eligibility checks speed up approvals

- Omnichannel notifications improve communication

- Self-service portals simplify repayments

- Predictive alerts help identify upsell and refinancing opportunities

Digital engagement also strengthens risk management. Early warning systems detect repayment stress sooner and take proactive action before delinquency increases.

Embedded finance ecosystems are also creating new acquisition channels for lenders by integrating credit experiences directly into digital platforms, payment ecosystems, and mobile-first borrower journeys. Explore how Rishabh Software developed a secure mobile payment app that enabled seamless digital transactions, improved financial access, and increased mobile money adoption.

How Rishabh Software Builds Digital Lending Platforms That Perform

Building a digital-first lending platform is not an IT upgrade project. It is a strategic transformation, and the architectural decisions made in the first six months determine the institution’s competitive trajectory for the next decade.

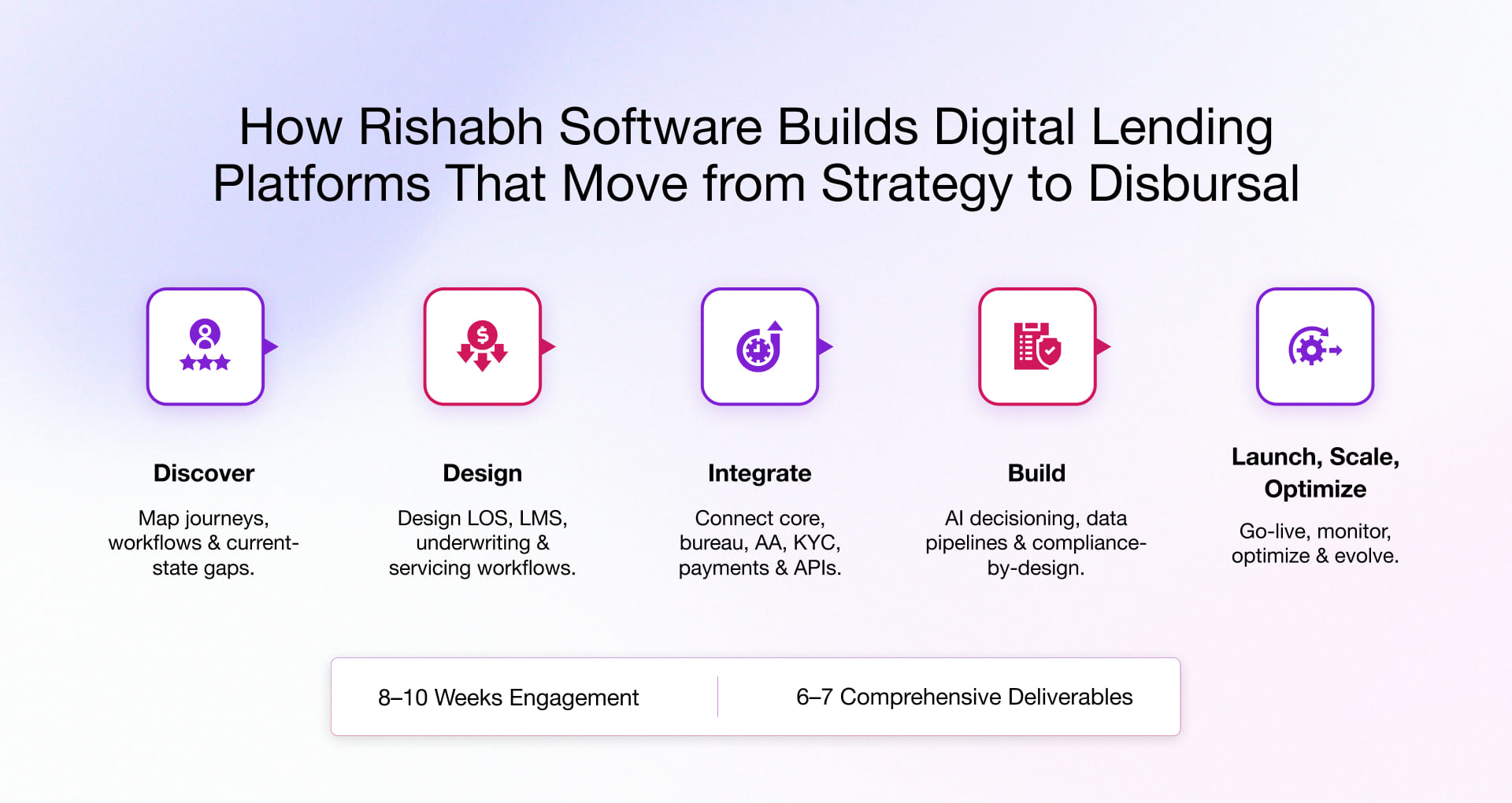

Our Digital Lending Engagement Approach from Strategy to Disbursal

Step 1: Discover

- Map borrower journeys, credit workflows, and current-state gaps across origination, underwriting, servicing, and collections.

- Stakeholder interviews, pain point mapping, and integration landscape review completed in Weeks 1–2.

Step 2: Design

- Build LOS, LMS, underwriting, and servicing workflow blueprints tailored to your credit policy, borrower segments, and regulatory environment.

- Journey definition for borrowers, agents, underwriters, and admins. Weeks 3–4.

Step 3: Integrate

- Connect core digital lending banking systems, bureau, Account Aggregator, KYC/AML, payments, and partner APIs into a unified lending architecture.

- Target architecture design and AI, data, and reporting requirements finalized. Weeks 5–6.

Step 4: Build

- Develop AI-assisted decisioning with explainability, alternative data pipelines, and compliance-by-design controls engineered from Sprint 1.

- MVP backlog and prioritized implementation roadmap with effort and cost estimates. Weeks 7–8.

Step 5: Launch, Scale, Optimize

- Phased go-live, optional clickable prototype and post-launch performance monitoring

- Ongoing platform evolution as regulatory and market requirements change. Weeks 9–10 and beyond.

Engagement duration: 8–10 weeks from Discovery to MVP-ready blueprint. 6–7 comprehensive deliverables.

Rishabh Software has successfully served banks, NBFCs, fintechs, and credit enterprises to engineer full-stack digital lending systems. Neither templates nor rebranded SaaS deployments. We build systems around how your borrowers behave, what your credit policy demands, and where your growth needs to go.